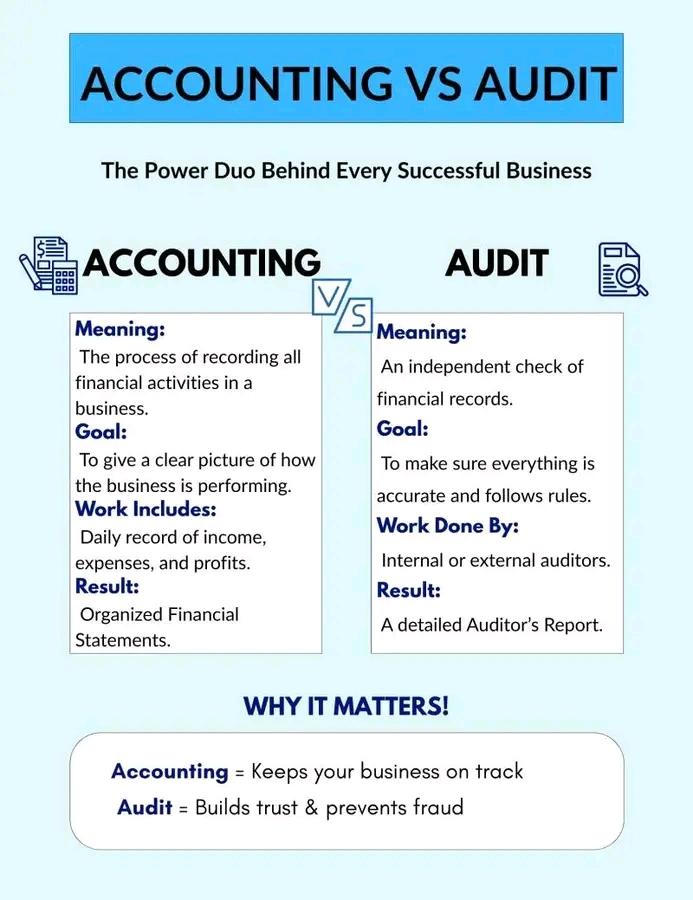

ACCOUNTING VS AUDITING VS FINANCE

ACCOUNTING:

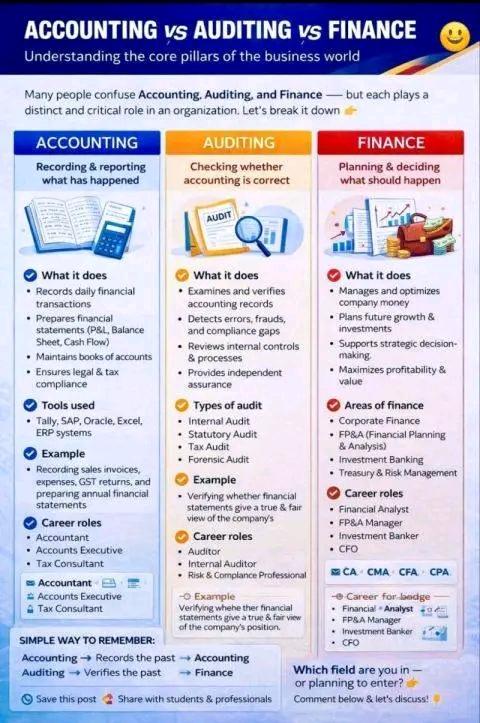

Accounting is the systematic recording and reporting of financial transactions. It ensures the business has accurate books and financial statements.

Key activities:

• Recording daily transactions

• Preparing trial balance

• Preparing financial statements

• Managing payables/receivables

• Costing, budgeting, payroll

Source: Accounting involves recording and processing financial data systematically.

AUDITING:

Auditing is the independent examination of financial statements to ensure they are accurate and comply with standards.

Key activities:

• Checking internal controls

• Verifying transactions and balances

• Ensuring compliance with IFRS/ISA

• Issuing an audit opinion

Source: Auditing verifies that financial data is correct and compliant with standards.

FINANCE:

Finance deals with managing money, making investment decisions, and planning for the future.

Key activities:

• Capital budgeting

• Investment analysis

• Risk management

• Funding decisions (debt vs equity)

• Cash flow forecasting

Source: Finance is not about recording or verifying — it is about using money to create value.

Simple Way to Remember

• Accounting = Record the numbers

• Auditing = Check the numbers

• Finance = Use the numbers to make decisions

ACCOUNTING:

Accounting is the systematic recording and reporting of financial transactions. It ensures the business has accurate books and financial statements.

Key activities:

• Recording daily transactions

• Preparing trial balance

• Preparing financial statements

• Managing payables/receivables

• Costing, budgeting, payroll

Source: Accounting involves recording and processing financial data systematically.

AUDITING:

Auditing is the independent examination of financial statements to ensure they are accurate and comply with standards.

Key activities:

• Checking internal controls

• Verifying transactions and balances

• Ensuring compliance with IFRS/ISA

• Issuing an audit opinion

Source: Auditing verifies that financial data is correct and compliant with standards.

FINANCE:

Finance deals with managing money, making investment decisions, and planning for the future.

Key activities:

• Capital budgeting

• Investment analysis

• Risk management

• Funding decisions (debt vs equity)

• Cash flow forecasting

Source: Finance is not about recording or verifying — it is about using money to create value.

Simple Way to Remember

• Accounting = Record the numbers

• Auditing = Check the numbers

• Finance = Use the numbers to make decisions

🔶 ACCOUNTING VS AUDITING VS FINANCE 🔶

🔊 ACCOUNTING: ⬇️

👉 Accounting is the systematic recording and reporting of financial transactions. It ensures the business has accurate books and financial statements.

➡️ Key activities: 👇

• Recording daily transactions

• Preparing trial balance

• Preparing financial statements

• Managing payables/receivables

• Costing, budgeting, payroll

▪️ Source: Accounting involves recording and processing financial data systematically.

🔊 AUDITING: ⬇️

👉 Auditing is the independent examination of financial statements to ensure they are accurate and comply with standards.

➡️ Key activities:

• Checking internal controls

• Verifying transactions and balances

• Ensuring compliance with IFRS/ISA

• Issuing an audit opinion

▪️ Source: Auditing verifies that financial data is correct and compliant with standards.

🔊 FINANCE: ⬇️

👉 Finance deals with managing money, making investment decisions, and planning for the future.

➡️ Key activities:

• Capital budgeting

• Investment analysis

• Risk management

• Funding decisions (debt vs equity)

• Cash flow forecasting

▪️ Source: Finance is not about recording or verifying — it is about using money to create value.

🧠 Simple Way to Remember

• Accounting = Record the numbers

• Auditing = Check the numbers

• Finance = Use the numbers to make decisions

·56 Views

·0 Reviews